When LIC launches a new insurance plan, it naturally attracts attention from policyholders, investors, and insurance advisors across India. The newly introduced LIC Jeevan Saathi 888 Plan is no exception. Designed specifically for married couples, this plan combines joint life insurance protection with a one-time investment structure and guaranteed benefits.

For many families, managing multiple insurance policies can become complicated over time. LIC has attempted to simplify this by offering a joint life insurance policy where both husband and wife are covered under a single plan. Since it is a single premium policy, there is no need to worry about paying yearly, quarterly, or monthly premiums after the initial purchase.

However, the most important question remains: Is LIC Jeevan Saathi 888 actually worth buying, or is it simply another traditional insurance plan with limited returns?

In this detailed review, we will examine the plan’s features, benefits, maturity value, death benefits, suitability, and potential drawbacks so that you can make an informed decision.

Also see: LIC Jeevan Sathi 889 Plan Details

LIC Jeevan Saathi 888 at a Glance

| Feature | Details |

|---|---|

| Plan Name | LIC Jeevan Saathi 888 |

| Plan Type | Joint Life Endowment Plan |

| Premium Payment | Single Premium |

| Risk Coverage | Husband and Wife Both Covered |

| Minimum Sum Assured | ₹3,00,000 |

| Maximum Sum Assured | Subject to Underwriting |

| Policy Term | 10, 15, 20, 25 Years (depending on option selected) |

| Guaranteed Addition | ₹70 per ₹1,000 Basic Sum Assured per year |

| Loan Facility | Available |

| Surrender Facility | Available |

| Market Linked | No |

| Bonus Based | No |

| Launch Date | 1 June 2026 |

What Makes LIC Jeevan Saathi 888 Different?

Most traditional LIC policies cover only one life. If both husband and wife want protection, they usually need separate policies. The biggest difference with LIC Jeevan Saathi 888 is that both spouses are insured under one policy contract.

Another important feature is the single premium structure. Instead of paying premiums every year, the policyholder pays the entire premium amount once at the beginning. After that, the policy continues for the selected term without any future premium obligations.

This combination of joint life coverage, guaranteed additions, and one-time payment makes the plan particularly attractive to families that prefer simplicity and certainty over market-linked investments.

Also see: SBI Children’s Fund Review

Who Can Buy LIC Jeevan Saathi 888?

The plan is primarily designed for legally married couples. The minimum entry age starts at 18 years, while the maximum entry age depends on the option selected.

Under Option 1, the maximum entry age can go up to 60 years. Under Option 2, the maximum age limit is lower, making it more suitable for younger couples seeking higher life cover.

The minimum basic sum assured starts at ₹3 lakh, while the maximum sum assured depends on the applicant’s income profile and underwriting requirements.

How Does LIC Jeevan Saathi 888 Work?

The working mechanism is straightforward.

You select the desired sum assured and policy term. After paying the single premium, the policy remains active throughout the chosen term. During this period, both lives remain covered according to the policy conditions.

If both policyholders survive till maturity, LIC pays the maturity benefit. If either spouse dies during the policy term, death benefits become payable as per the selected option.

Unlike ULIPs or market-linked insurance plans, the policy does not depend on stock market performance. This means the benefits are more predictable and easier to calculate.

Understanding the Guaranteed Addition Benefit

One of the biggest attractions of LIC Jeevan Saathi 888 is its guaranteed addition feature.

According to the plan structure, policyholders receive a guaranteed addition of ₹70 per ₹1,000 of Basic Sum Assured for every policy year completed.

This feature significantly increases the maturity value over the long term.

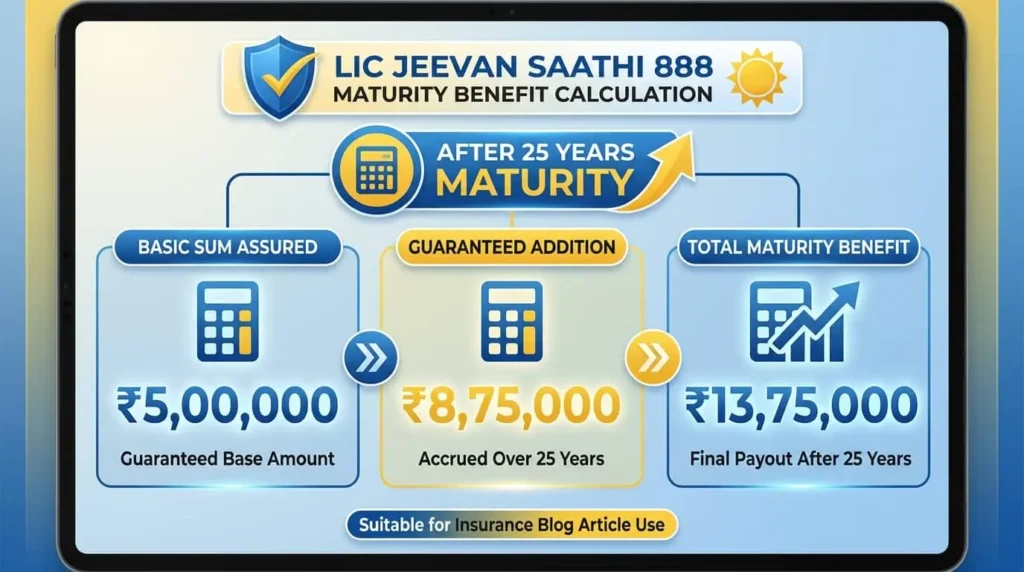

For example, suppose a couple chooses a basic sum assured of ₹5 lakh and a policy term of 25 years.

The annual guaranteed addition would be:

₹5,00,000 ÷ ₹1,000 × ₹70 = ₹35,000 per year

Over 25 years, the guaranteed addition accumulates to approximately ₹8,75,000.

This amount is added to the maturity proceeds, making the final payout considerably larger than the original sum assured.

LIC Jeevan Saathi 888 Maturity Benefit Example

Let us understand the maturity benefit using a practical example.

Assume:

- Husband Age: 30 Years

- Wife Age: 28 Years

- Basic Sum Assured: ₹5,00,000

- Policy Term: 25 Years

At maturity, if at least one life survives until the end of the policy term, the benefits may include:

- Basic Sum Assured: ₹5,00,000

- Guaranteed Addition: ₹8,75,000

Estimated Total Maturity Benefit: ₹13,75,000

For conservative investors who prefer guaranteed outcomes, this predictability can be more appealing than uncertain market-linked returns.

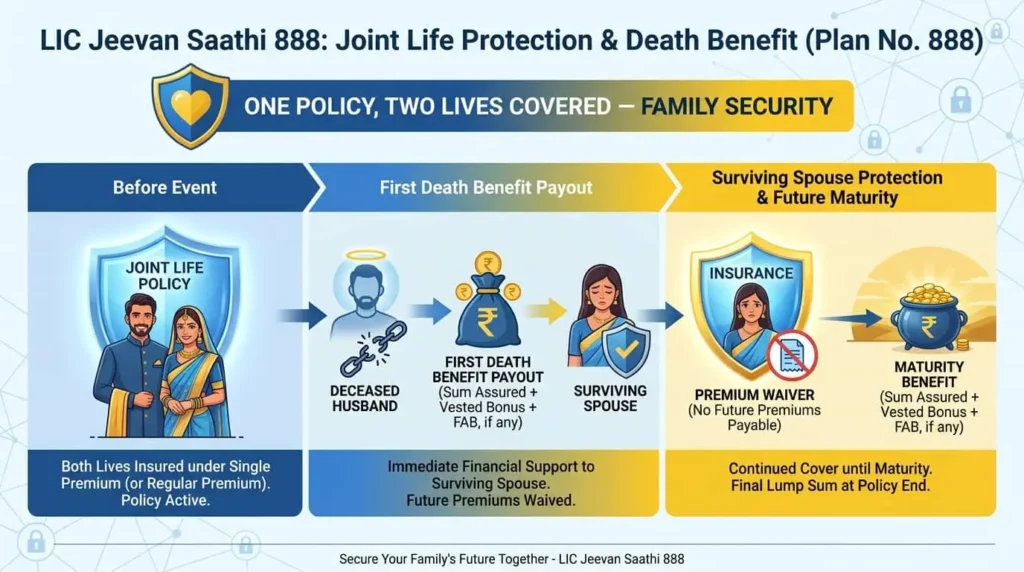

What Happens If One Spouse Dies?

This is where the joint life structure becomes important.

Suppose the husband dies during the fifth policy year. In such a situation, LIC pays the applicable death benefit based on the selected death benefit option.

After receiving the death benefit, the policy can continue for the surviving spouse. If the surviving spouse remains alive until maturity, the maturity benefit may still become payable according to the policy terms.

This feature ensures that financial support is available immediately after the first death while still preserving future benefits for the surviving partner.

What Happens If Both Spouses Die?

If both insured persons die during the policy term, the nominee becomes eligible to receive the death benefits according to the policy conditions.

In addition to the applicable sum assured on death, accumulated guaranteed additions up to that point are considered while determining the final benefit payable.

This ensures that the family receives meaningful financial protection even in the worst-case scenario.

Additional Riders Available Under LIC Jeevan Saathi 888

Insurance plans are often evaluated not only on their basic coverage but also on the additional protection they offer. LIC Jeevan Saathi 888 allows policyholders to strengthen their coverage through optional riders.

One of the available options is the Accidental Death and Disability Benefit Rider. If the insured person dies due to an accident, an additional rider benefit may become payable over and above the base policy benefits. Similarly, in case of permanent disability caused by an accident, the rider can provide additional financial support.

The second major option is the Term Assurance Rider. This rider works similarly to a traditional term insurance cover and provides extra life protection for a relatively small additional cost.

For young couples with dependent children or financial liabilities such as home loans, these riders can significantly improve overall protection.

Loan Facility: Can You Borrow Against the Policy?

Many policyholders prefer insurance products that offer liquidity during emergencies. LIC Jeevan Saathi 888 addresses this concern by providing a loan facility.

Once the policy acquires the required value and satisfies the applicable conditions, policyholders can apply for a loan against the policy. According to the available plan details, the loan facility becomes available after a specified period from policy commencement.

This feature can be useful during temporary financial difficulties because it allows policyholders to access funds without surrendering the policy completely.

However, it is important to remember that unpaid policy loans and interest may reduce the final benefits payable under the policy.

Surrender Value and Early Exit Option

Life circumstances can change over time. Some investors may require access to their money before policy maturity.

LIC Jeevan Saathi 888 offers a surrender facility, which means policyholders can exit the plan before maturity if required.

However, like most traditional insurance plans, surrendering early may not always provide the best financial outcome. The surrender value depends on factors such as policy duration, premium paid, and applicable surrender value calculations.

Therefore, this plan should ideally be purchased with a long-term commitment in mind rather than as a short-term investment product.

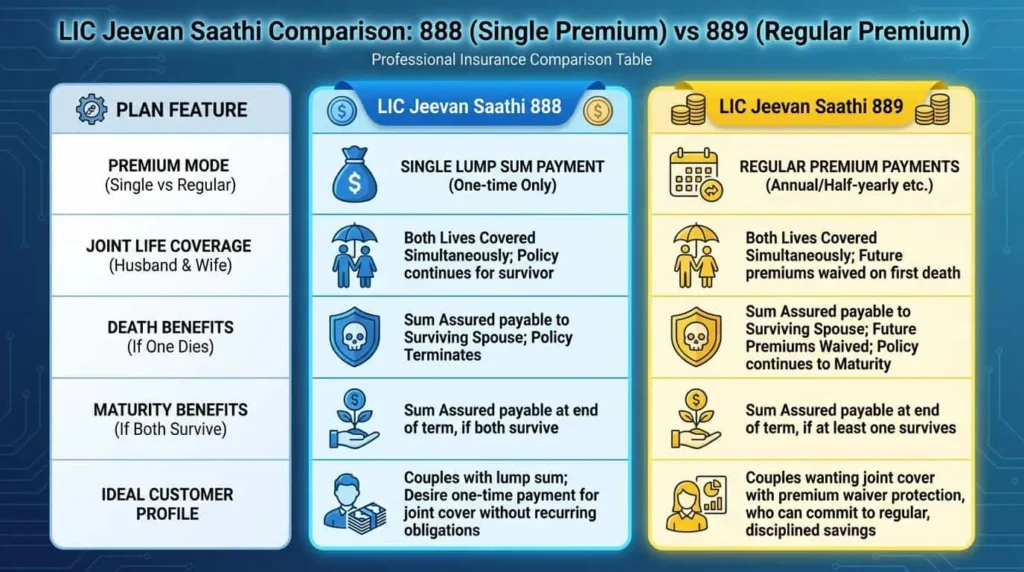

LIC Jeevan Saathi 888 vs LIC Jeevan Saathi 889

Many readers are currently comparing LIC Jeevan Saathi 888 and LIC Jeevan Saathi 889 because both plans were introduced around the same time and target married couples.

While LIC Jeevan Saathi 888 is designed as a single premium joint life plan, LIC Jeevan Saathi 889 follows a different premium payment structure and may suit couples who prefer spreading their premium payments over time instead of making a large one-time investment.

If you are looking for a detailed comparison between both plans, you can read our guide on LIC Jeevan Saathi 889 Plan Details, where we explain premium structures, benefits, and suitability in depth.

For investors with surplus funds available today, Plan 888 may appear more convenient because there is no future premium burden. On the other hand, couples who want to preserve liquidity may find Plan 889 more practical.

Who Should Consider Buying LIC Jeevan Saathi 888?

Not every insurance plan is suitable for every investor. The right choice depends on financial goals, risk appetite, and liquidity requirements.

LIC Jeevan Saathi 888 may be suitable for:

- Married couples seeking a single policy for both lives.

- Investors looking for guaranteed benefits rather than market-linked returns.

- Individuals who prefer a one-time investment instead of recurring premiums.

- Families that want insurance protection and savings benefits within the same policy.

- Conservative investors who prioritize capital preservation and predictability.

The plan may be especially attractive to retired individuals or near-retirement investors who have access to a lump sum amount and want a structured insurance solution.

Who May Want to Explore Other Options?

Although the plan has several strengths, it may not be the perfect choice for everyone.

Young investors primarily focused on wealth creation may find equity-based investments more rewarding over very long periods. Similarly, individuals seeking maximum life insurance coverage at the lowest cost may find pure term insurance more efficient.

Before investing, it is important to ask a simple question:

“Am I buying this plan mainly for insurance protection, guaranteed savings, or both?”

The answer can help determine whether LIC Jeevan Saathi 888 aligns with your financial objectives.

Key Advantages of LIC Jeevan Saathi 888

The strongest advantages of the plan include:

- Joint life coverage under a single policy.

- One-time premium payment.

- Guaranteed addition throughout the policy term.

- Predictable maturity benefits.

- Availability of riders.

- Loan and surrender facilities.

- Suitable for conservative investors.

These features make the plan different from many traditional individual life insurance products available in the market.

Potential Limitations to Consider

Every financial product has trade-offs, and LIC Jeevan Saathi 888 is no exception.

A few points investors should evaluate carefully include:

- Large upfront investment requirement.

- Lower liquidity compared to some other investment options.

- Returns may not match long-term equity investments.

- Best suited for investors seeking stability rather than aggressive growth.

Understanding both strengths and limitations helps buyers make informed decisions rather than relying solely on promotional material.

Final Verdict: Is LIC Jeevan Saathi 888 Worth Buying?

LIC Jeevan Saathi 888 introduces an interesting concept for Indian married couples by combining joint life insurance, guaranteed additions, and a single premium structure within one policy.

The plan is not designed to compete with high-growth investments. Instead, it focuses on providing financial security, predictable benefits, and convenience for couples who value certainty.

If your priority is market-beating returns, other investment avenues may deserve consideration. However, if you prefer a combination of insurance protection and guaranteed long-term benefits with a one-time investment, LIC Jeevan Saathi 888 can be a meaningful addition to your financial portfolio.

As with any insurance product, comparing it with your existing coverage, financial goals, and family needs before purchasing is always advisable.

Frequently Asked Questions (FAQs)

What is LIC Jeevan Saathi 888?

LIC Jeevan Saathi 888 is a joint life single premium insurance plan designed for married couples. It provides life insurance coverage to both husband and wife under a single policy.

Is LIC Jeevan Saathi 888 a market-linked plan?

No. It is a non-linked insurance plan and is not affected by stock market fluctuations.

How many times do I need to pay the premium?

The premium is paid only once at the beginning of the policy.

What is the minimum sum assured under LIC Jeevan Saathi 888?

The minimum basic sum assured is ₹3 lakh.

Does LIC Jeevan Saathi 888 offer guaranteed returns?

The plan offers guaranteed additions, which increase the overall maturity benefit.

Can I take a loan against LIC Jeevan Saathi 888?

Yes, the policy includes a loan facility subject to LIC’s applicable terms and conditions.

Is LIC Jeevan Saathi 888 better than LIC Jeevan Saathi 889?

Both plans serve different purposes. Plan 888 is suitable for investors looking for a one-time investment option, while Plan 889 may be more suitable for those who prefer regular premium payments.

What happens if one spouse dies during the policy term?

The applicable death benefit becomes payable according to the selected option, while the surviving spouse may continue to receive future policy benefits as per policy conditions.

Disclaimer: This article is intended for informational and educational purposes only. Policy features, benefits, eligibility conditions, premiums, and returns may change as per LIC guidelines. Readers should verify the latest policy details from LIC or a qualified insurance advisor before making any financial or insurance-related decision.